India Electricity Planning

India is the world’s most populous country and the fourth largest economy. It is also the third biggest producer of electricity and carbon emitter. As it continues to expand its energy access and industrial base, the demand for reliable, affordable, and clean electricity will grow rapidly. Recognizing this challenge, India has committed to achieving carbon neutrality by 2070.

In collaboration with the Prayas (Energy Group) and Sylvan Energy Analytics, the project advances India’s decarbonization efforts through open-source datasets, models, and analyses that strengthen planning and capacity building at both national and state levels.

Jump to section

Key Findings

Electricity system costs decline over time, even while meeting ambitious long-term carbon targets. Our results show that, across a range of technology and demand assumptions, overall system costs fall relative to current levels, including under conservative cost scenarios.

Cost-optimal clean energy deployment exceeds the official near-term 2030 target. Under conservative assumptions, renewables supply the majority of electricity, supported by large-scale batteries, while achieving meaningful emissions reductions.

Climate policies or clean energy targets are essential in the long-term to meet ambitious carbon mitigation and net-zero goals. Climate policies or clean energy targets are essential to meet a 90% carbon emissions reduction goal, which will make India's carbon neutrality goal by 2070 increasingly attainable.

Dashboard

Overview: India in 2020

GridPath-India, built using the open-source GridPath power systems modeling platform, is an open-source electricity system planning and operations model. The GridPath-India model has a spatial resolution of 34 load zones associated with an hourly demand profile, one for each state and union territory, and one for the neighboring country of Bhutan, a major hydropower exporter to India .

Fossil fuels, including coal, natural gas, and oil, dominate India's existing electricity system, generating 74.9% of total electricity demand in 2020. That year, coal alone accounted for 235 GW (or 60.3% of total) installed capacity and 994TWh (or 71.4% of total) energy generation. An additional 12.6 GW of coal capacity has been built since 2020 until 2025 and 24.2 GW being planned and expected to be constructed by 2030, all of which we include in the 2030 coal capacity in our model.

Existing generation capacity mix (2020) and interstate transmission corridors

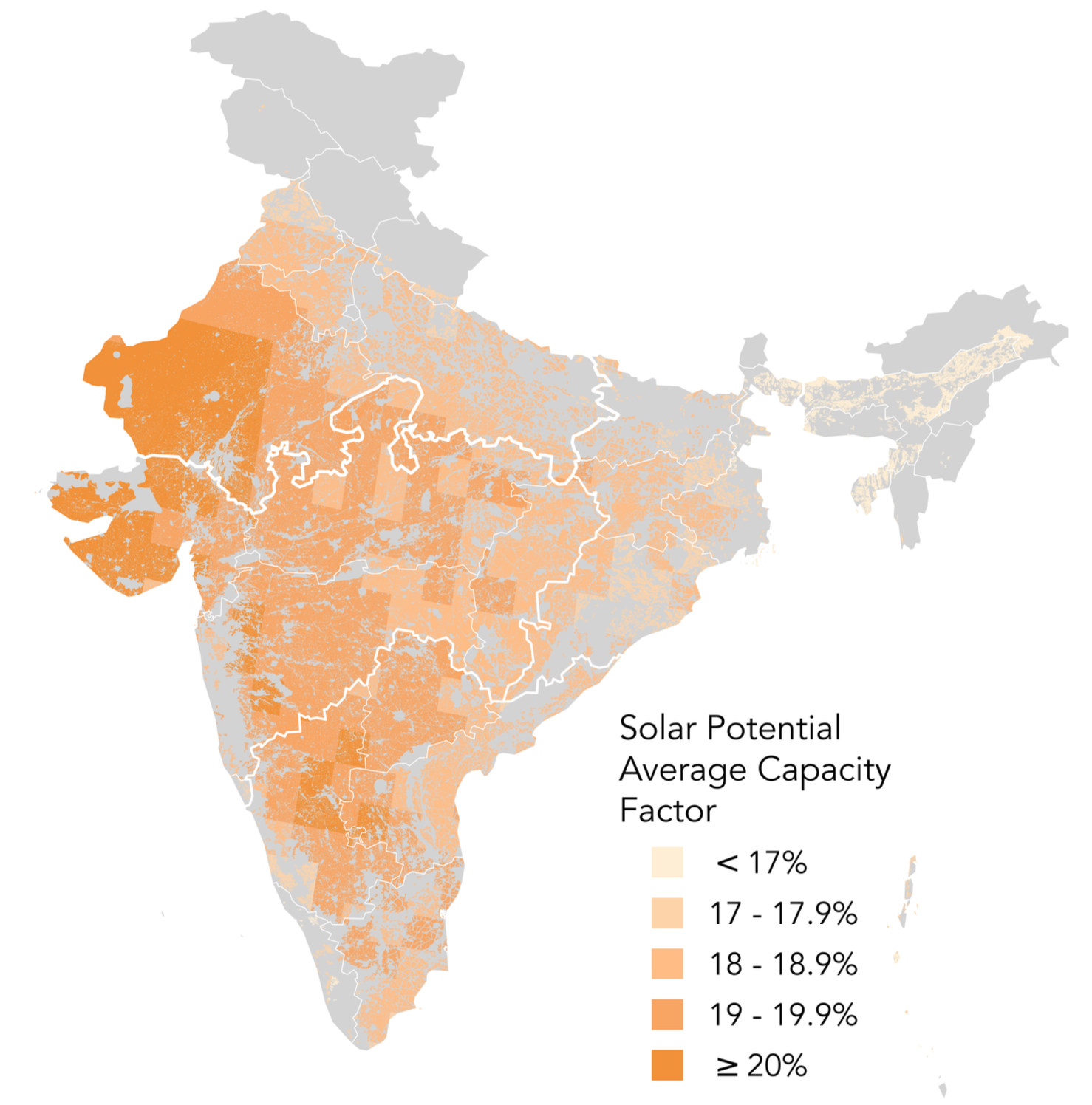

Solar PV resource average capacity factors

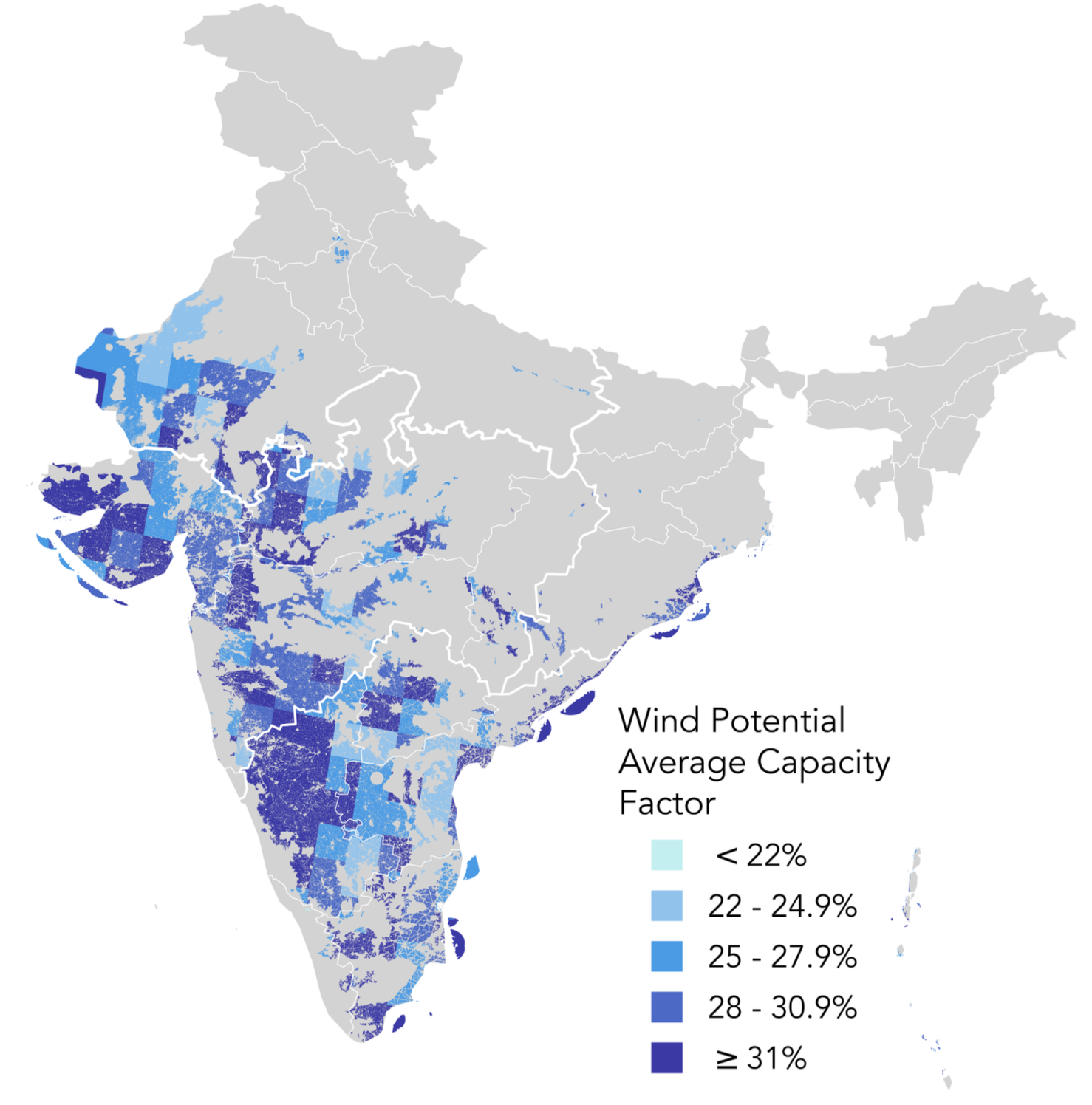

Onshore and offshore wind resource average capacity factors

Capital cost projections from 2020-2050 for onshore and offshore wind, rooftop, single-axis, and fixed-tilt solar PV, coal, combined cycle gas turbine, combustion turbine, hydropower (run-of-river), nuclear, battery storage, hydrogen storage, and pumped hydro storage.

State-wise electricity generation by resource (stacked bars) and electricity demand (circles) in 2020

Costs, emissions and clean-energy shares

Scenarios are evaluated based on system costs and GHG emissions for their relevance to consumer costs and climate mitigation. While total system costs increase with electricity generation growth, cost per unit of energy matters to consumers

Costs include generation, storage, and interstate transmission investment and operations. Intrastate transmission and distribution costs are assumed similar across scenarios. All costs are in real 2020 USD or INR controlling for inflation.

For GHG emissions, total emissions compare against 2020 levels while emissions intensity measures the climate impact per unit of generation.

We also examine the clean energy share in total electricity generation.

Across the technology cost scenarios, only 36.5 GW of coal capacity is built by 2050. The coal fleet's energy generation falls as the share of low variable cost renewable energy generation increases. In contrast, solar PV, wind, and battery storage technologies dominate new infrastructure investments across all scenarios.

VRE (wind and solar) capacity increases from an existing 72 GW in 2020 to 421GW in 2030 to meet India's official non-fossil target of 500 GW. From 2030, VRE capacity more than triples to ~1,510 GW by 2040, and then doubles (1.9 times) to ~2,902 GW to achieve a 90% carbon emissions reduction by 2050.

Cost optimal capacity deployment and energy generation

Changing costs with increased decarbonization

As electricity demand grows with India’s economic development, total power system costs increase over time, more than doubling by 2040 and rising further by 2050. Despite this growth, real electricity costs per MWh remain lower than 2020 levels across all future investment periods and technology cost assumptions.

Technology costs for solar, wind, and battery storage strongly influence overall system costs. Higher VRE and storage costs lead to higher system costs in later years, while lower cost trajectories reduce total costs and enable deeper emissions reductions with limited additional expense. Under lower-cost assumptions, the system can achieve high carbon mitigation targets more affordably.

As low variable-cost wind and solar expand and fossil generation declines, variable costs fall accordingly. Coal-related variable costs initially rise through 2030 but decline sharply by 2040 and 2050, reflecting coal’s reduced energy generation role and increasing function as capacity for system reliability.

The GridPath-India model is an open-source electricity system planning and operations model with 34 load zones, one for each state and union territory plus Bhutan, and hourly demand profiles.

The model includes existing, planned, and candidate generation and storage projects. Over 1,300 candidate wind and solar sites were identified through a spatially explicit, multi-criteria site suitability analysis. Transmission is limited by inter-state transfer capacities but intra-state transmissions are ignored.

Using two representative days per month (peak and median demand) at hourly temporal resolution, we co-optimize generation, storage, and transmission investments and operations across four investment periods (2020 to 2050) that each represent 10 years.

The 2020 period represents the existing system, whereas the 2030, 2040, and 2050 periods represent near-term, medium-term, and long-term futures. The model then fixes new investments and runs a unit commitment and dispatch (production cost) model over 8,760 hours to ensure system reliability.

GridPath-India Model

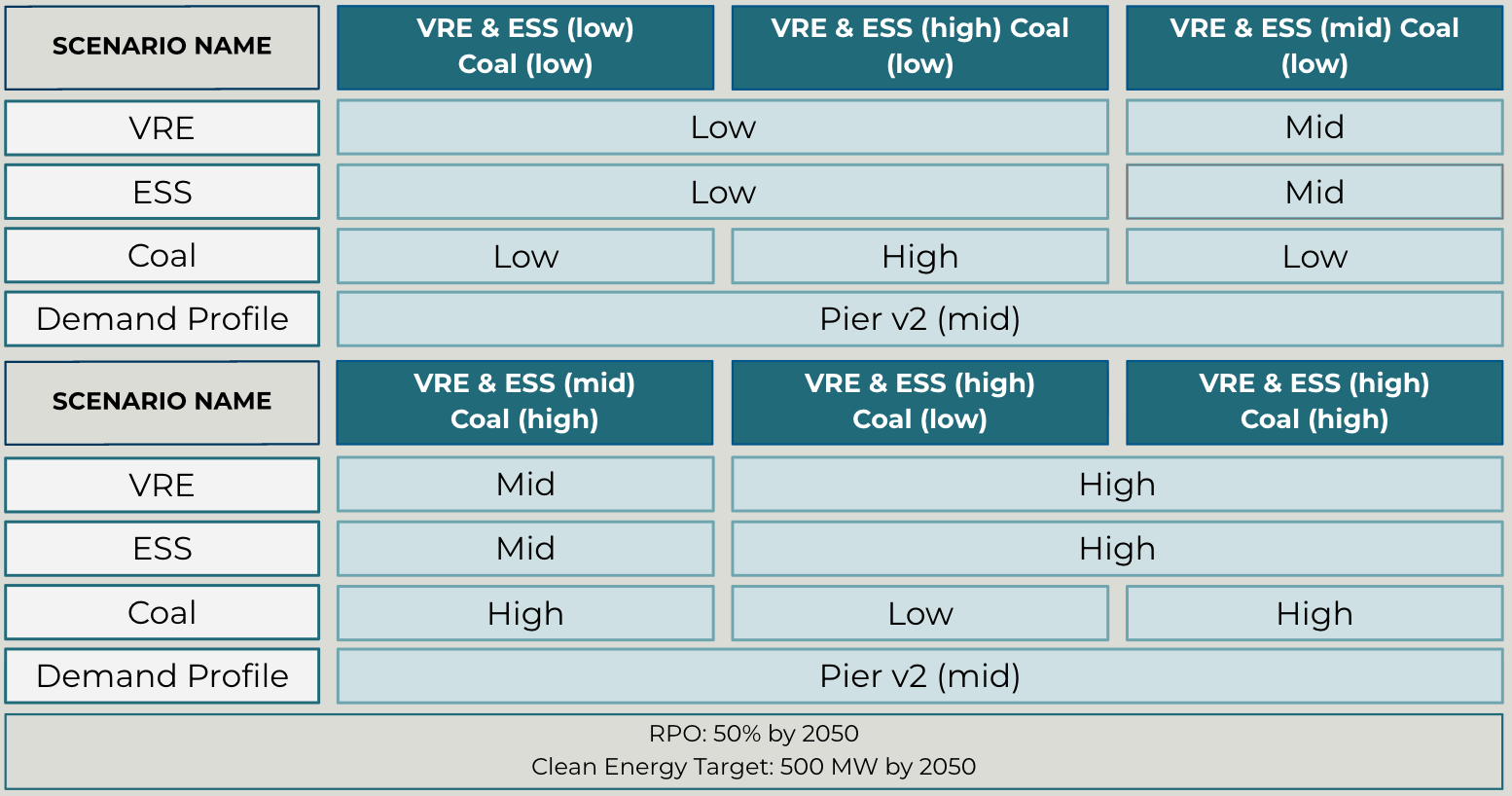

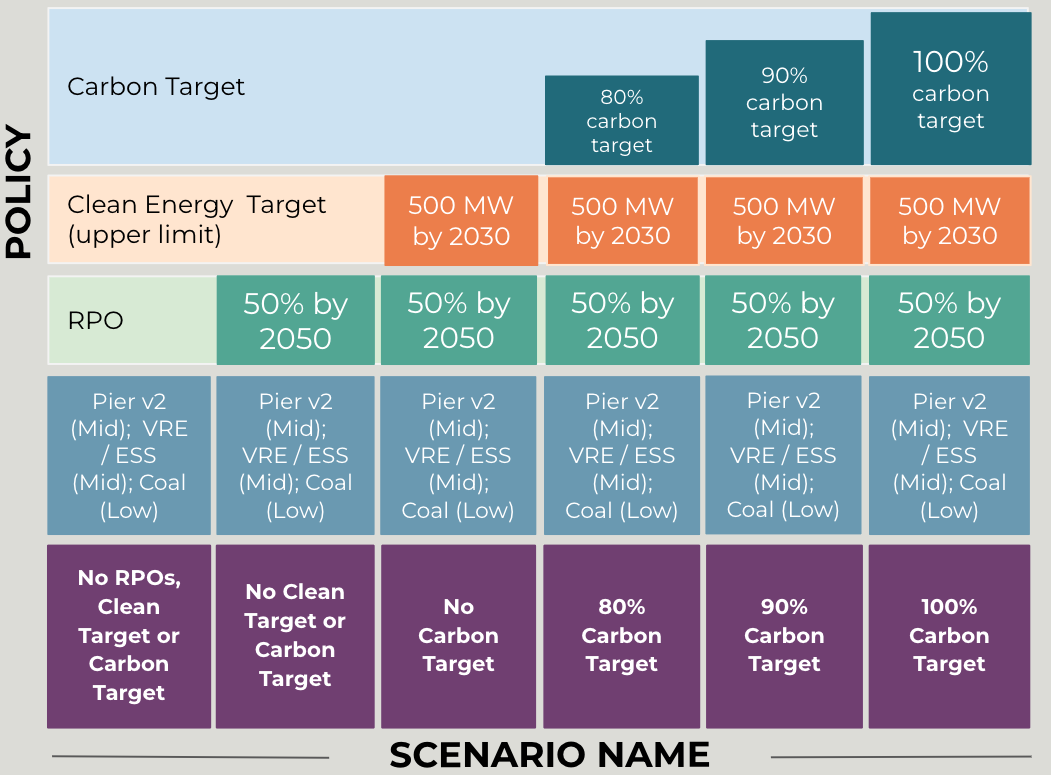

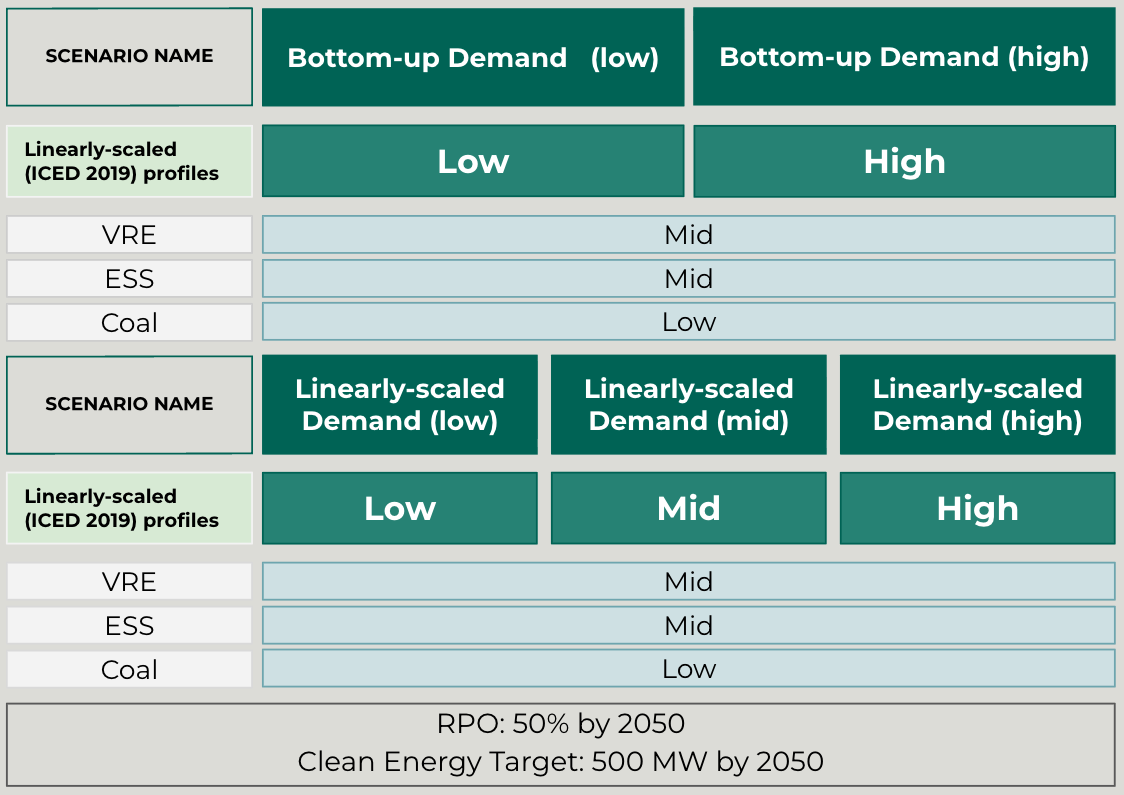

Scenarios

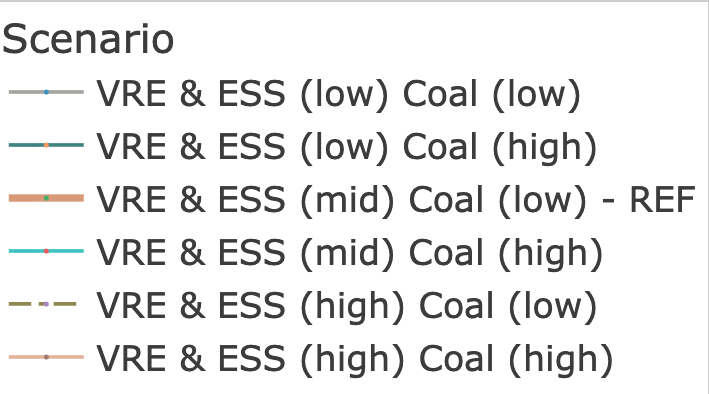

The technology cost scenarios consider low/mid/high variable renewable energy (VRE) and energy storage system (ESS) costs, and low/high supercritical coal.

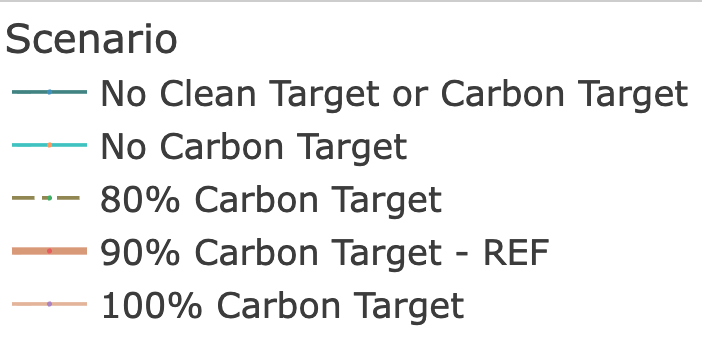

The policy scenarios include the enacted policies of a 500 MW clean-energy generation capacity target by 2030, and explore 80%, 90%, and 100% CO2 emission reduction targets from 2020 levels by 2050.

The demand scenarios consider low/mid/high demand scenarios from bottom-up or linearly-scaled approaches.

Data

Coming Soon

Publication & Research Outputs

-

Coming soon

Team

emLab, University of California at Santa Barbara

Ranjit Deshmukh

Associate Professor

Guillermo Terren-Serrano

Postdoctoral Scholar

Abhishek Sharma

Postdoctoral Scholar

Shradhey Prasad

Project Manager

Measrainsey Meng

Postdoctoral Scholar

Sarah Erickson

Communications Specialist